Building a balanced EV fleet in a changing market

Rhys Whitcombe, Director, BCF Wessex Consultants

The UK fleet market is entering a new phase of electrification. It’s one defined by the pace of transition but even more so by the breadth of zero-emission OEMs and models now available.

Alongside established OEMs, a growing number of newer, lower-cost EV manufacturers, many with roots in China, are gaining traction. According to the Society of Motor Manufacturers and Traders (SMMT), battery electric vehicles now account for around one in five new car registrations in the UK, with challenger brands rapidly increasing their share of that growth. Fleet operators, under pressure to decarbonise while controlling costs, are being offered greater choice, but with more complexity.

The question has moved way beyond whether or not to electrify; it’s now about how to balance the electric cars within a fleet. Here are five practical steps to help fleet managers make more informed, balanced decisions.

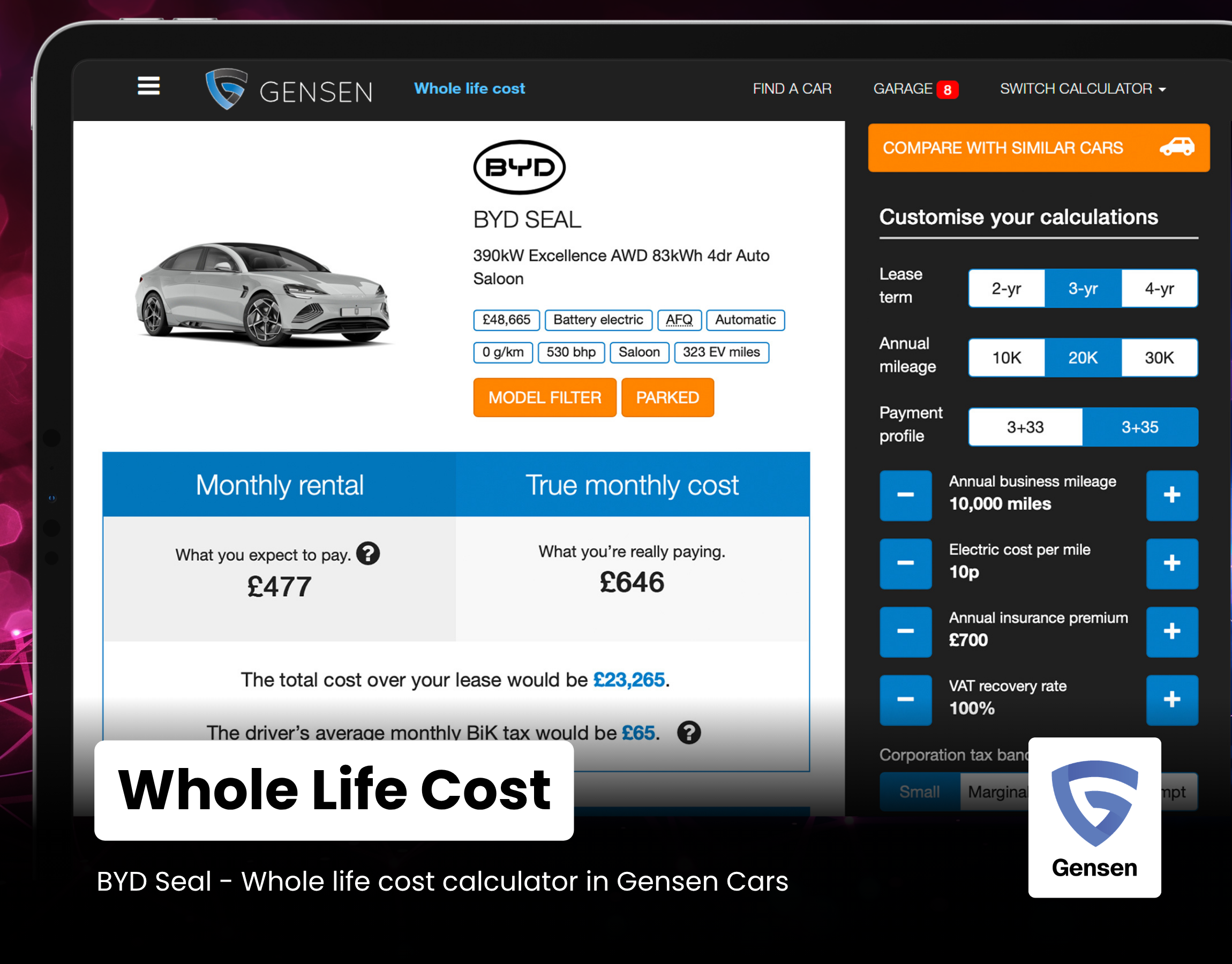

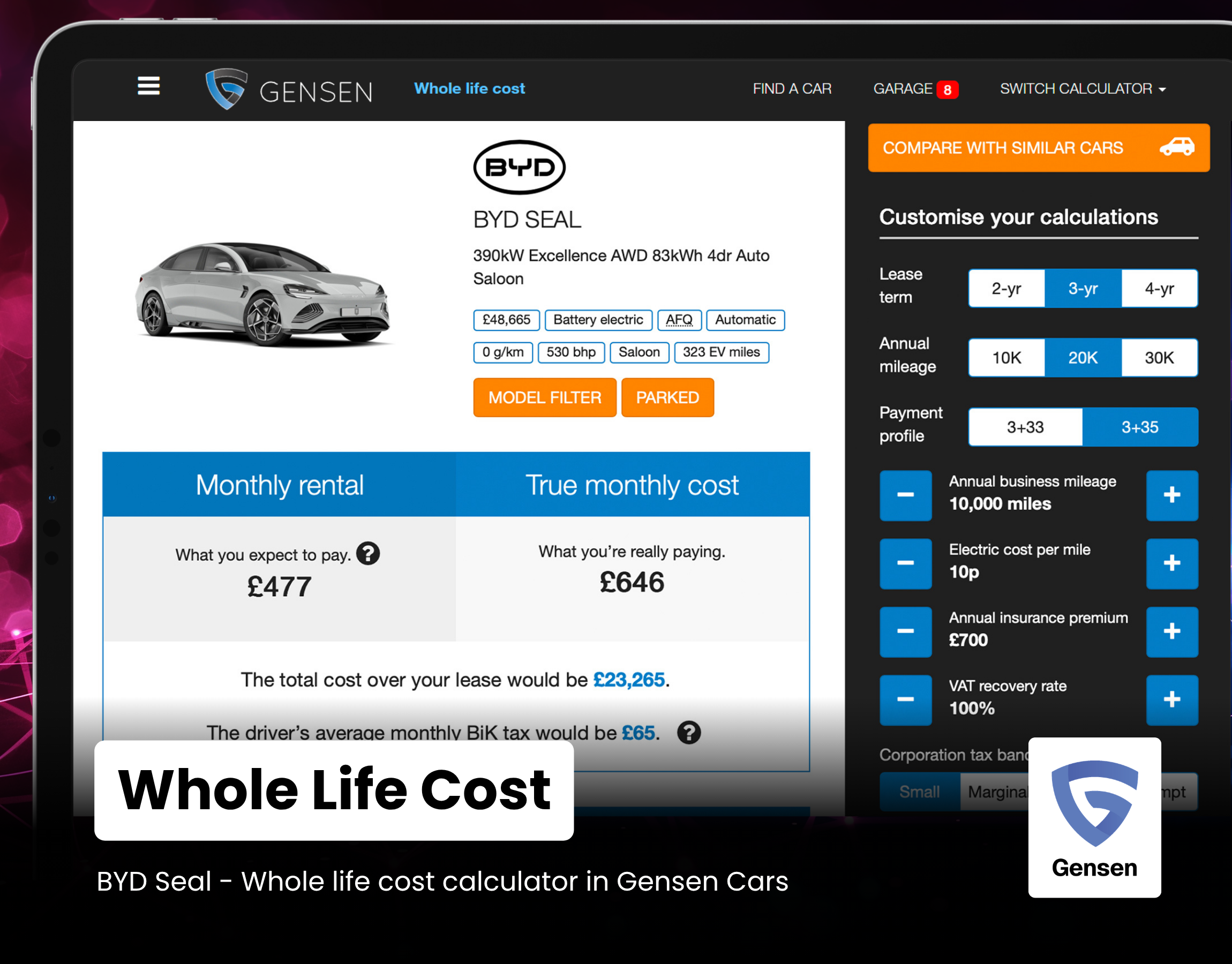

1. Look past the headline price; focus on whole life cost

Lower headline prices are attractive, especially under budget pressure, but they rarely tell the full story. Whole life cost (WLC), inclusive of tax, rentals, maintenance, fuel or energy costs, and insurance, remains the most accurate way to assess true value.

Then, factors such as Benefit-in-Kind (BiK) tax, Class 1A NIC, and efficiency can outweigh any upfront saving.

This is particularly relevant with newer EV entrants, some of whom are generating record-breaking growth upon entering the UK market. Competitive pricing from brands like BYD and Jaecoo is driving strong interest, but the real differentiator is how those vehicles perform over time.

For example, when using our Gensen WLC calculator, we instantly see that a high-spec BYD Seal can deliver WLC savings of up to £240 per month against a comparable BMW i4, despite only a modest difference in list price, thereby emphasising why WLC, not headline cost, should drive decision-making.

2. Match vehicle choice to driver aspiration, not brand perception

Fleet composition should always start with role requirements. Range, charging access, and driver usage patterns will often matter more than the manufacturer badge.

In my conversations with leasing market colleagues, newer EV entrants seem to be gaining traction in quite specific segments, particularly younger drivers or those in more cost-sensitive roles. Established brands may still hold an advantage in areas such as trust, perceived quality, or driver appetite.

The key is segmentation, matching vehicles to role and use case, avoiding a one-size-fits-all approach. Notably, newer EV entrants are resonating with drivers, combining strong technology and interior quality, and in some cases attracting more interest than established brands like Volkswagen, Audi and BMW.

Opening schemes up to a wider range of OEMs ensures that both newer and established brands are used where they deliver the most value.

Table: SMMT New Car Data - Top 25 brands (YTD - April 2026)

| Rank | Marque | Units | Market share |

|---|---|---|---|

| 1 | Volkswagen | 59,878 | 7.84% |

| 2 | Kia | 43,538 | 5.70% |

| 3 | BMW | 42,607 | 5.58% |

| 4 | Ford | 41,004 | 5.37% |

| 5 | Audi | 38,133 | 4.99% |

| 6 | Mercedes | 35,285 | 4.62% |

| 7 | Vauxhall | 33,729 | 4.41% |

| 8 | MG | 30,883 | 4.04% |

| 9 | Skoda | 30,675 | 4.01% |

| 10 | Toyota | 30,389 | 3.98% |

| 11 | Peugeot | 30,386 | 3.98% |

| 12 | Hyundai | 30,278 | 3.96% |

| 13 | Nissan | 28,839 | 3.72% |

| 14 | BYD | 26,396 | 3.45% |

| 15 | Land Rover | 25,313 | 3.31% |

| 16 | Volvo | 24,117 | 3.16% |

| 17 | Renault | 23,645 | 3.09% |

| 18 | Jaecoo | 22,789 | 2.98% |

| 19 | MINI | 18,814 | 2.46% |

| 20 | Cupra | 15,171 | 1.99% |

| 21 | Tesla | 12,570 | 1.65% |

| 22 | Omoda | 12,324 | 1.61% |

| 23 | Citroen | 12,142 | 1.59% |

| 24 | Mazda | 11,669 | 1.53% |

| 25 | Chery | 10,977 | 1.44% |

Showing the top 10 brands on mobile. View on desktop for the full ranking.

3. Recognise the risks: Review, support and supply

The EV market is both maturing and evolving rapidly. New entrants often jump to the front of mind with competitive pricing, but fleet managers should be careful; new entrants may not offer the reassuring reputation of more established brands. When looking at newer, less established brands, fleet managers should consider the following:

Residual value assumptions and volatility, and how these impact monthly lease rentals.

Whether to allow employees to select used EVs as a lower-cost option.

Aftersales, service support, warranties and manufacturer coverage.

The lack of data about real-life living with new entrant models.

Manufacturer’s global stability and long-term UK presence.

These factors don’t override the case for newer entrants, but they reinforce that cost alone isn’t enough. Real-driver feedback highlights mixed experiences, from driving feel to software reliability, making due diligence for drivers and fleet managers essential.

Encouragingly, brands like BYD, Jaecoo and Omoda are rapidly expanding UK dealer networks, strengthening aftersales support, with each offering access to more than 100 dealerships nationwide. However, challenges remain with research from earlier this year highlighting some insurers are still reluctant to cover certain models, adding another layer of risk for fleet managers to consider.

4. Align funding strategy with vehicle mix

Vehicle choice and funding methods are closely linked but often considered separately.

Different funding approaches, be they contract hire, contract purchase, employee car ownership or even salary sacrifice for all, can materially change the cost structure of a fleet vehicle. For example, lower-cost EVs may perform particularly well within a salary sacrifice scheme where employee affordability is a key driver.

At the same time, a broader vehicle mix often requires more flexible funding. For example, drivers covering high mileage or operating in areas with limited charging may still favour employee car ownership schemes utilising petrol, diesel or hybrid cars, especially following the recent generational increase to Approved Mileage Allowance Payments. However, as these schemes become less attractive over time, cash allowances that support personal leasing may be a more practical alternative until universal charging enables EVs to operate practically throughout the country.

Fleet managers who align funding strategy with vehicle mix and driver needs are better positioned to unlock the true financial benefit of the full spectrum of market options.

5. Build flexibility into your fleet policy

Perhaps the most important step is recognising that the market will continue to change and likely at pace.

New manufacturers and models are entering the UK. Pricing structures are evolving. Government policy and taxation will continue to shift; for example, will eVED be introduced in 2028 or deferred until 2032, as called for by the BVRLA and AFP?

What looks like the optimal fleet mix today may shift dramatically over the next year or two.

Fleet policies should therefore be designed with flexibility at their core:

Allowing for multiple vehicle tiers or categories in certain areas.

Enabling regular review of approved vehicle lists.

Incorporating data-led decision-making rather than fixed assumptions.

These ensure fleets can adapt quickly as the market develops.

Key takeaways for fleet managers

The growth of lower-cost EV options is a positive development for the fleet sector. It introduces greater competition, broadens access to electrification, and creates new opportunities to manage costs.

For fleet managers, the challenge goes beyond choosing between “new” and “established” brands but understanding where each fits within a coherent, cost-effective strategy.

Here are my top five recommendations to help build that strategy:

Adopt whole-life cost as the primary decision metric; look beyond the headline figure!

Segment your fleet by role and usage, not by brand preference.

Assess risk alongside cost when it comes to new, lesser-known brands, particularly around integration and support infrastructure.

Align funding strategy with vehicle choice to maximise fleet efficiency.

Build flexibility into your fleet policy to respond to a fast-moving market.

Contact us if you would like to discuss any of the content on this page.